- 9847209977 / 790252232

Middle East – VAT

VAT Registration Guide

VAT Timeline

31 October 2017

Businesses with an annual turnover exceeding AED 150 million should apply for registration by 31 October 2017

30 November 2017

Businesses with an annual turnover exceeding AED 10 million should apply for registration by 30 November 2017

4 December 2017

All other business entities with an annual turnover exceed the mandatory registration threshold (AED 375,000) should apply for registration by 4 December 2017

Who is required to register for VAT

AED 375,000

Mandatory registration threshold*: AED 375,000

AED 187,500

Voluntary registration threshold*: at least AED 187,500

*Threshold will be calculated as follows >>

Threshold will be calculated as follows:

– Total value of supplies made by a taxable person for the previous 12 months; or

– Total value of supplies of the subsequent 30 days

– Value of exempted supplies will not be considered for computing the annual supplies

No threshold applies to non established taxable persons – they may be required to register

Taxable supply definition >>

For the purposes of understanding whether a registration obligation exists, a taxable supply refers to a supply of goods or services made by a business in the UAE that may be taxed at a rate of either 5% or 0%. Imports are also taken into consideration for this purpose, if a supply of such goods or services would be taxable if made within the UAE.

A business must register for VAT if the total value of its taxable supplies and imports within the UAE exceeds the mandatory registration threshold of AED 375,000, either during the previous 12 months or within the upcoming 30 days.

A business can voluntarily register for VAT if the total value of its taxable supplies and imports within the UAE exceeds the voluntary registration threshold of AED 187,500, either during the previous 12 months or within the upcoming 30 days.

A business can also register voluntarily if its expenses exceed the voluntary registration threshold.

A business can also register voluntarily if its expenses exceed the voluntary registration threshold.

A non-resident doing taxable business in the UAE needs to register for VAT regardless of the above-mentioned thresholds.

If a company has multiple entities that trade with each other, it is possible to register as a VAT group. In a group registration, all of the entities within the VAT group are treated as one entity for VAT purposes. The supplies made between members of a VAT group are disregarded (no VAT is due on them). The supplies made by the VAT group to an entity outside the VAT group are subject to normal VAT rules. When a company registers as a VAT group, it receives a single TRN and will file a single VAT return.

How to register for VAT?

Business can register through the e-Services portal on the FTA website.

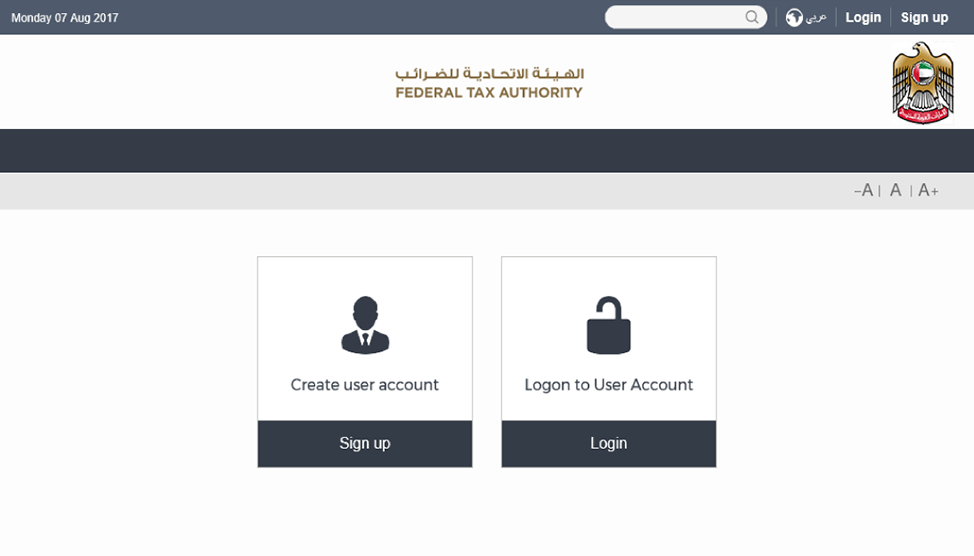

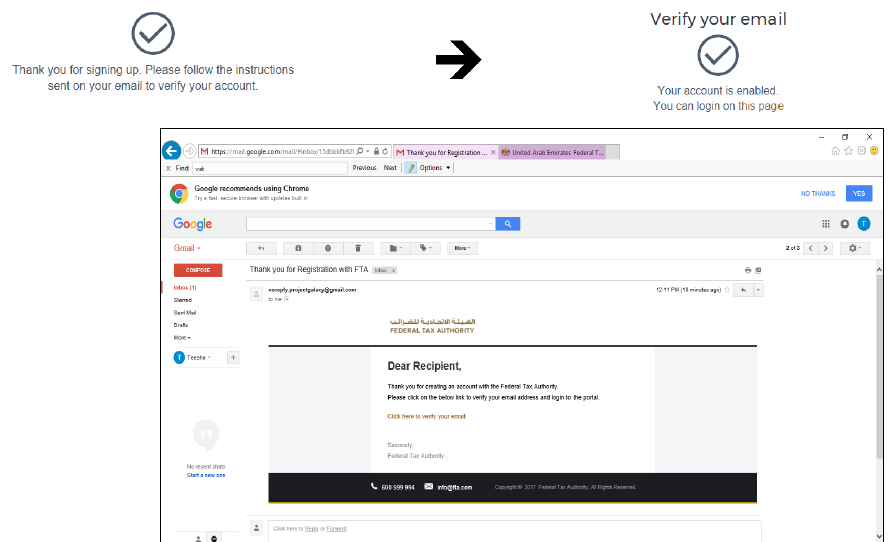

Step 1

1. Open the VAT registration portal on FTA website and create a user account.

The first time you access the portal you will be required to register your details.

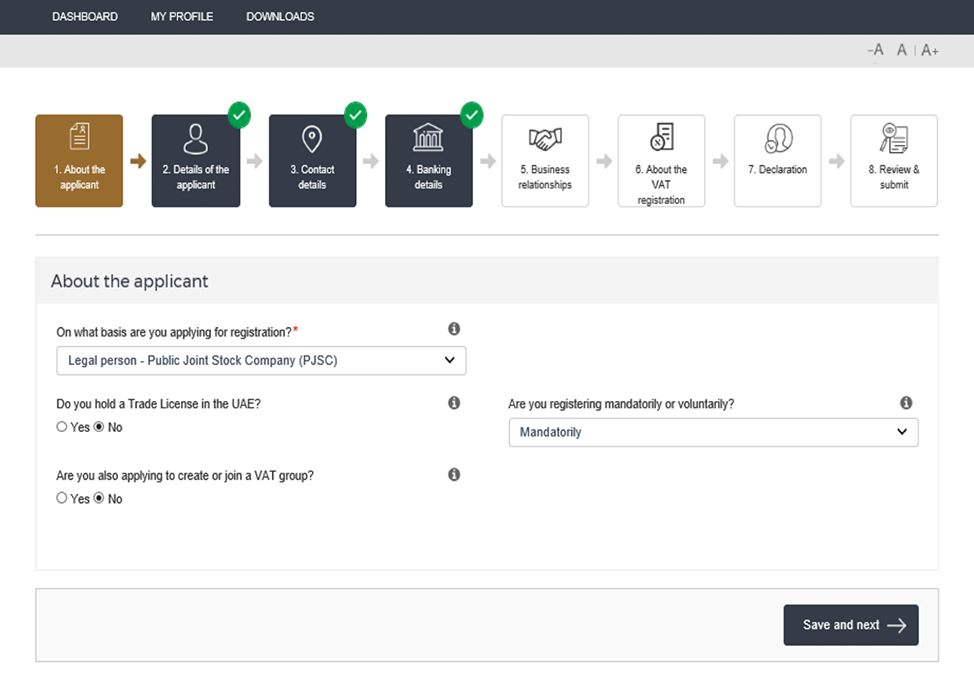

What are the supporting documents/details required to register under VAT

Make your company comply with VAT regulations

VAT Law requirements:

Face VAT Confidently With No.1 VAT Accounting Software for UAE

Easy- to-use & Affordable Full-Cycle Accounting from Day One:

- Comprehensive financial and tax accounting in one system;

- Advanced bookkeeping and payroll functions;

- Automatic VAT calculation;

- One-click reporting;

- Complete audit and tax compliance.

MaxSell Accounting solution ensures you always have ready-to-use VAT features throughout the accounting cycle in compliance with any new VAT rates or regulations.

Learn how a VAT-ready accounting software will help you comply with the UAE's VAT regulations.

Source: The UAE's Federal Tax Authority Website

Copyright 2026 Syosys InfoTech Private Limited.

Search engine

Use this form to find things you need on this siteCart

No products in the cart.